In This Article

- What a Modern Mortgage POS Actually Does

- Five Features That Cut Pre-Qualification From Days to Minutes

- AUS Integration: The Speed Multiplier

- MortgageExchange: The POS to LOS to Core Spine

- Calyx PointCentral: The ABT-Hosted LOS Option

- Microsoft 365 Copilot Business for Pre-Qual Workflows

- Agentic AI Market Context

- ROI Framework: Measuring POS Impact

- Technical Reference

- Frequently Asked Questions

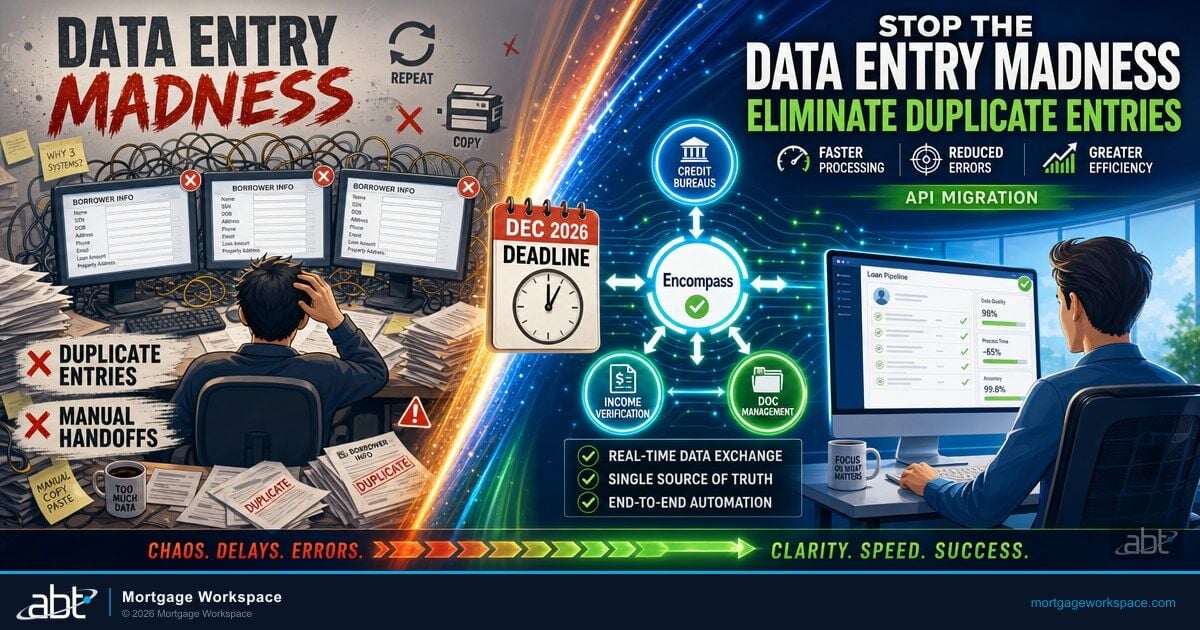

The phrase "weeks to minutes" is real, but most of the weeks do not live where mortgage operations teams think they do. Independent mortgage banks, mortgage brokers, and hybrid LO shops usually look first at the Point-of-Sale interface when pre-qualification feels slow. The POS is the front door, and a modern POS does help. The actual weeks, though, come from the seams between the POS, the loan origination system, the document management surface, and the borrower communication channels. A borrower fills out the application in minutes. The pre-qualification decision lands on the loan officer's desk three days later because verified data had to be re-keyed, the AUS submission had to be staged in another tool, and the borrower update email had to be drafted by hand in Outlook.

The mortgage POS software market hit $1.14 billion in 2026 and is on pace for $2.31 billion by 2032 at a 12.3 percent compound annual growth rate. That is the vendor side of the story. The institution side of the story is different. The mortgage companies cutting pre-qualification from weeks to minutes are not just buying a faster POS. They are pairing a modern POS with a mortgage-aware integration spine that carries verified data from the POS into the LOS without re-keying, a tenant-locked AI assistant that reviews the file inside the institution's own Microsoft 365 boundary, and an LOS environment that the institution does not have to operate itself. This article walks through the speed features a modern POS should deliver, the integration architecture that makes the "weeks to minutes" claim survive contact with a real boarding feed, and the way ABT MortgageExchange, ABT-hosted Calyx PointCentral, and Microsoft 365 Copilot Business fit together in production for mortgage companies that have already standardized on Microsoft 365.

What a Modern Mortgage POS Actually Does

A mortgage Point-of-Sale system is the borrower-facing application portal where the loan journey begins. Traditional versions were digital paper forms. Modern POS interfaces are active processing engines that verify data, pull credit, and push files to underwriting before the borrower closes the browser tab.

The difference matters. A static form collects information. An intelligent POS interface validates it, cross-references it against third-party data sources, and routes it into the loan origination system in real time. That gap between collect and process is where days disappear from the pipeline.

For mortgage companies running ICE Encompass, Calyx Path, MeridianLink Mortgage Access, or Encompass Consumer Connect, POS integration quality determines whether data flows or stalls. The best platforms use modern APIs to maintain bidirectional sync, so loan officers see verified borrower data the moment it hits their queue. Mortgage companies running Calyx PointCentral as the LOS get the same pattern with the additional benefit that the LOS itself is operated by ABT on Microsoft Azure rather than the institution running it on its own hardware.

Five Features That Cut Pre-Qualification From Days to Minutes

Automated Data Verification

Modern POS platforms connect directly to credit bureaus, employment verification services, and asset verification providers. When a borrower enters information, the system pulls and validates data in the background. No manual re-keying. No waiting for a processor to call an employer.

Platforms like Plaid, Argyle, and Truv provide real-time income and asset verification through consumer-permissioned data. This replaces the old method of uploading pay stubs and waiting for manual review. For mortgage companies, the verified data is only as useful as the integration that carries it into the LOS, which is where the spine described later in this article matters.

Intelligent Document Capture

Optical Character Recognition paired with AI reads uploaded documents, extracts key fields, and flags missing information on the spot. Borrowers get instant feedback instead of a phone call three days later asking for page two of their bank statement.

AI-powered document processing now handles over 700 document types with 97.8 percent classification accuracy in a peer-reviewed study processing 1.2 million pages of mortgage documents. For mortgage companies, the practical value is fewer borrower call-backs for missing items and a cleaner file arriving at the underwriter's desk.

Real-Time Status Tracking

Borrowers expect the same transparency they get from package tracking. Modern POS platforms provide a centralized hub with automated notifications via email, text, or push notification. Every milestone triggers an update. Every missing item generates a specific request. Loan officers stop spending three hours a day answering "where is my application" calls.

Mobile-First Architecture

Sixty percent of borrowers engage in mortgage activities from mobile devices. A POS that does not work on a phone is not a POS. Leading platforms let borrowers start on desktop during lunch and finish on mobile from the couch, with full state preservation across devices.

Dual AUS Submission

The fastest POS platforms now run both Fannie Mae's Desktop Underwriter and Freddie Mac's Loan Product Advisor at the point of application. Loan officers compare findings side by side and select the best outcome for each borrower without running separate submissions. The dual-submission pattern shaves another half day off the pre-qualification window for AUS-eligible files.

AUS Integration: The Speed Multiplier

The single biggest accelerator in pre-qualification is direct AUS connectivity. Once the POS collects and verifies borrower data, it submits to an Automated Underwriting System and returns a decision in minutes.

This is where the "weeks to minutes" transformation actually happens. Manual pre-qualification requires a loan officer to review the file, a processor to verify documents, and an underwriter to assess risk. AUS integration compresses those steps into a single automated workflow. Research from the Federal Reserve Bank of New York shows fintech lenders close mortgages 20 percent faster than traditional lenders with lower default rates. The speed comes from automation, not shortcuts.

For mortgage company operations teams, AUS integration means loan officers spend time building relationships instead of chasing documents. Processors handle exceptions, not routine verifications. Underwriters focus on complex files, not checkbox reviews. The integration spine that carries the AUS findings into the LOS and out to the borrower communication surfaces is what determines whether that operational gain shows up in pull-through and capacity metrics or stalls at the next handoff.

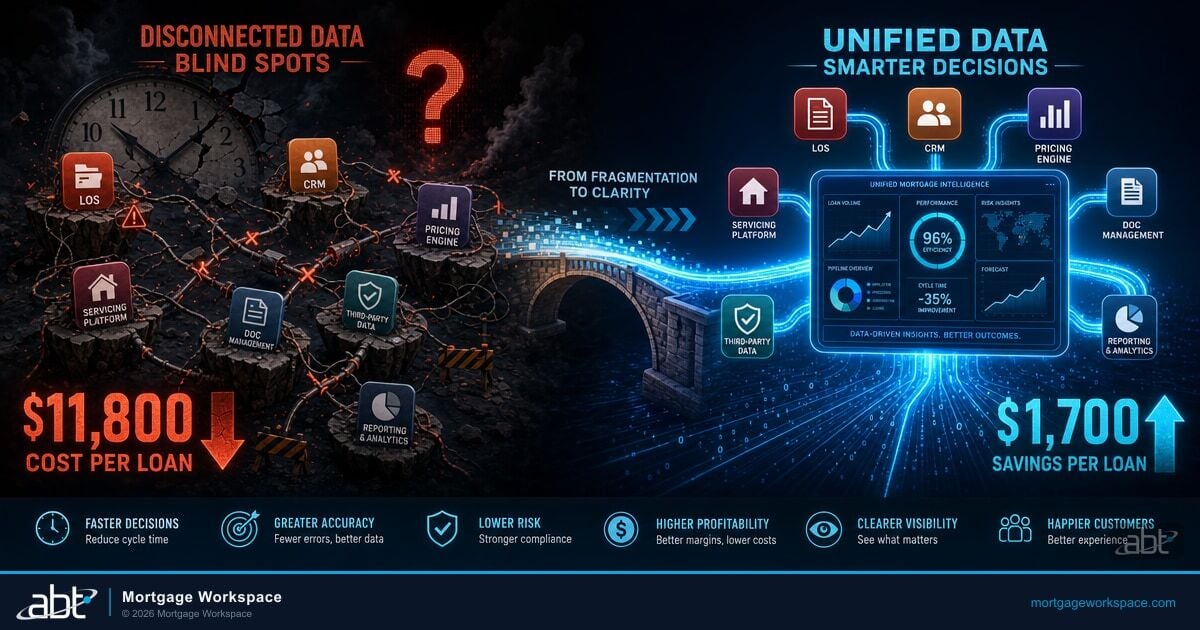

MortgageExchange: The POS to LOS to Core Spine

POS modernization is half the answer. The other half is the integration spine that carries verified borrower data from the POS into the LOS, out to the borrower communication channels, and into post-funding servicing systems without anyone typing the same field into a second tool. ABT MortgageExchange is the mortgage-aware integration platform most ABT customers use for that spine.

| System Layer | What Flows Through MortgageExchange | Common Platforms Connected |

|---|---|---|

| Point-of-Sale | Borrower application data, verified income and asset feeds, dual AUS findings, document upload metadata, status events. | Encompass Consumer Connect, MeridianLink Mortgage Access, Calyx Path borrower portal, third-party POS platforms with API connectivity. |

| Loan Origination System | Pre-qualification decisions, conditions, disclosures, AUS findings, underwriting decisions, closing package events. | ICE Encompass, MeridianLink Mortgage, Mortgage Cadence, Dark Matter Technologies Empower, ABT-hosted Calyx PointCentral. |

| Borrower Communication and Document Surfaces | Status emails staged for loan officer review, condition request notifications, e-disclosure delivery events, document management updates. | Microsoft 365 Outlook, Microsoft 365 Teams, Microsoft SharePoint document libraries, e-signature platforms. |

| Audit and Reporting | Event log of every cross-system handoff, tamper-evident retention, evidence packages tied to CFPB, FFIEC, and investor delivery expectations. | Microsoft Fabric data lake, Microsoft Power BI dashboards, Microsoft Purview retention and audit policies. |

The mortgage-aware piece matters. Generic middleware platforms route messages between systems, but every mortgage-specific data mapping has to be built and maintained inside the platform by the institution. MortgageExchange ships with pre-built connectors and event handling for the LOS, document management, and borrower communication systems most ABT mortgage customers actually run, with the pre-qualification event, the disclosure event, the condition-cleared event, and the closing-package event all mapping to mortgage-aware schemas rather than being reconstructed by the mortgage company. Audit evidence collection runs by default. Our companion article on tracking your mortgage pipeline across the LOS, document, and BI surfaces walks through the integration pattern at the pipeline visibility layer.

Access Business Technologies manages Microsoft 365 tenants and hosts Microsoft Azure environments for 750 financial institutions, including independent mortgage banks, mortgage brokers, and hybrid LO shops on the MortgageWorkSpace footprint. The pattern across that footprint is consistent. The mortgage companies that compress pre-qualification from weeks to minutes do not just modernize the POS. They pair a modern POS with ABT MortgageExchange for the LOS spine, ABT-hosted Calyx PointCentral when the LOS itself needs to be operated as a service, and Microsoft 365 Copilot Business for the pre-qual review assist, all inside their existing Microsoft 365 tenant. Pre-qual throughput improves because Copilot reviews the file inside the M365 boundary instead of borrower data being copy-pasted into a consumer AI tool. Audit evidence improves because Microsoft Purview is retaining the right fields at the right cadence by default.

Calyx PointCentral: The ABT-Hosted LOS Option

Many mortgage companies on the MortgageWorkSpace footprint already run Calyx Path or Calyx PointCentral as their loan origination system. The split that matters for pre-qualification speed is operational. Calyx Path is the desktop product the mortgage company runs locally. Calyx PointCentral is the server product that gives multi-user access across loan officers, processors, and underwriters from a centralized origination environment. ABT hosts Calyx PointCentral on Microsoft Azure as a dedicated environment for mortgage companies that would rather have a Tier-1 Microsoft partner operate the LOS than maintain it on their own infrastructure.

The architecture matters for pre-qualification speed in three places. First, the POS-to-LOS connection lands in an environment ABT already monitors, so a feed that silently fails at 2 a.m. is caught before the next morning's pre-qualification queue runs against stale data. Second, the loan officer workstation, the borrower communication tooling, and the LOS share a Microsoft 365 identity layer through Microsoft Entra ID Conditional Access, so a loan officer logged in to Outlook is already authenticated against Calyx PointCentral with the same multi-factor posture. Third, the document management and the borrower communication surfaces live in the same Microsoft 365 tenant as the LOS access, which lets Microsoft 365 Copilot Business operate across the pre-qual file without crossing tenant boundaries.

ABT manages the PointCentral environment, the underlying Microsoft Azure compute and storage, the backup and disaster recovery configuration, and the patching cadence. The mortgage company owns the LOS data and the configuration. The combined surface is what most ABT mortgage customers describe when they say they have moved their LOS to ABT. Our companion article on running Encompass and Calyx for mortgage success covers the LOS operational pattern in more depth.

Microsoft 365 Copilot Business for Pre-Qual Workflows

The borrower experience compresses at the POS. The data flow compresses at MortgageExchange. The pre-qualification decision compresses inside Microsoft 365 Copilot Business, which is where the loan officer or processor actually reviews the file and stages the borrower communication. Copilot lives inside the mortgage company's Microsoft 365 tenant, governed by the same Microsoft Entra ID Conditional Access policies and Microsoft Purview data protection rules that already cover Outlook, Teams, and SharePoint. ABT manages the tenant. The mortgage company owns the data. Copilot reads only what the tenant grants it access to read.

In a pre-qualification workflow, Copilot opens the 1003 application from the LOS or document management surface, opens the income and asset statements, opens the credit report, and produces a structured pre-qual summary for the loan officer: borrower identity confirmed against the application, employer and income consistency confirmed against verification feeds, asset position confirmed against the statements, dual AUS findings extracted with the recommended outcome highlighted, and any flagged inconsistencies surfaced for review. The loan officer reviews the summary, accepts or overrides each finding, and approves the pre-qualification.

Key Takeaway

Copilot is not the underwriter. Copilot is the loan officer's review and communication assistant. Every pre-qualification decision is still made by a human with the file in front of them. The architectural difference is that the human is reviewing a structured summary instead of assembling one from five different screens, and the mortgage company can prove with audit evidence what Copilot read, what it summarized, and what the loan officer decided.

Copilot also handles the borrower-facing piece that usually slows a pre-qualification down. Drafting the conditional approval email from inside Outlook takes Copilot a few seconds against the borrower file already in the tenant. The loan officer reviews the draft, edits it, and sends it. The pre-qualification decision and the borrower communication both happen in the same Microsoft 365 tenant on the same loan officer workstation in the same loan officer session. The hand-off between deciding and communicating, which used to add a half day to the cycle, becomes a single review pass.

The tenant-locked nature of Copilot is the part that matters for regulators. Borrower data, including the loan applicant's NPI (Social Security number, income data, credit score, loan amount), never leaves the mortgage company's Microsoft 365 boundary. The pre-qualification summary Copilot drafts lives in the tenant. The borrower email Copilot stages is held for review inside Outlook before any send. The mortgage company retains full ownership of the data and full visibility into Copilot's actions through Microsoft 365 audit logging. For mortgage companies running Microsoft 365 Copilot Business or Microsoft 365 Copilot in the Business Premium tier, the licensing tier governs whether the company can scale Copilot to every loan officer versus a smaller pilot. The architecture, audit trail, and tenant boundary do not change.

Agentic AI Market Context

The 2026 POS market has moved beyond basic automation into agentic AI. In February 2026, Bevri launched an agentic AI-powered Point-of-Sale platform for NEXA Lending, the nation's largest mortgage brokerage. The system completes the 1003 application with the borrower, calculates and validates income and assets, runs dual AUS findings, and maps underwriting conditions to document requirements. Vendors including TidalWave and Zeitro have published comparable agentic capability claims. LenderLogix has published an evaluation framework for AI-powered POS claims that mortgage operations teams should review before any vendor demo.

The vendor agentic AI story is the market backdrop. The mortgage company side of the story is different. For a mortgage company already standardized on Microsoft 365 with ABT MortgageExchange carrying the integration spine and ABT hosting Calyx PointCentral as the LOS, the marginal cost of adding agentic capability to existing pre-qualification workflows through Microsoft 365 Copilot Business, Microsoft Copilot Studio, and Microsoft Power Automate is significantly lower than buying and integrating a third-party agentic POS, and the audit posture is cleaner because every agentic action runs inside the existing tenant boundary. Vendor agentic AI is real and useful. So is the agentic capability already sitting inside Microsoft 365 for mortgage companies that own a tenant they trust.

ROI Framework: Measuring POS Impact

Track these metrics before and after POS plus integration plus Copilot deployment to quantify the return:

- Application-to-pre-qualification time: Measure the hours or days from submission to decision. Modern POS plus MortgageExchange plus Copilot review cuts this from 3-5 days to under 30 minutes for AUS-eligible files.

- Application abandonment rate: Industry average is 75-80 percent. Mobile-optimized POS combined with real-time verification reduces abandonment by 25-40 percent.

- Manual touches per loan: Count every time a human re-enters or verifies data. Target: reduce by 60 percent or more. Most of the gain comes from the POS-to-LOS feed and the borrower communication automation, not the POS form itself.

- Loan officer capacity: Measure loans per LO per month. Vendor benchmarks indicate 2.5x faster pre-qualifications and 7-plus hours saved per file when POS automation, AUS integration, and Copilot review run together.

- Pull-through rate: Track applications submitted to applications funded. Faster pre-qualification with consistent borrower communication materially raises pull-through, which is the metric independent mortgage banks and brokers actually compensate against.

- Compliance error rate: Manual processes show 10-15 percent defect rates. Automation plus mortgage-aware integration plus Microsoft Purview governance brings this below 3 percent in practice.

Run these numbers against the current baseline. The ROI case usually pays for itself within the first quarter of deployment, but the durable gain comes from pull-through and borrower communication quality, not from the borrower-facing form speed alone.

Technical Reference

- Mortgage POS (Point-of-Sale): Borrower-facing application interface that collects, verifies, and routes loan data into origination systems.

- AUS (Automated Underwriting System): Fannie Mae's DU and Freddie Mac's LPA. Algorithmic engines that evaluate borrower risk and return approve, refer, or deny decisions.

- OCR (Optical Character Recognition): AI technology that reads scanned documents and extracts structured data fields.

- Agentic AI: Autonomous AI systems that execute multi-step workflows, make context-aware decisions, and resolve exceptions without human intervention.

- API-first architecture: System design pattern where all functionality is exposed through standardized Application Programming Interfaces, enabling real-time integration between platforms.

- ABT MortgageExchange: Mortgage-aware integration platform with pre-built connectors for ICE Encompass, MeridianLink Mortgage, Mortgage Cadence, Dark Matter Empower, and Calyx PointCentral against borrower communication and document management surfaces in Microsoft 365. Runs on Microsoft Azure, monitored and supported by ABT, audit evidence collected by default.

- Calyx PointCentral (ABT-hosted): The server edition of Calyx Software's loan origination platform, operated by ABT on Microsoft Azure for mortgage companies that want a Tier-1 Microsoft partner to run the LOS. Integrates through MortgageExchange and authenticates against the mortgage company's Microsoft Entra ID tenant.

- Microsoft 365 Copilot Business: Microsoft's tenant-locked AI assistant for small and mid-sized businesses, including independent mortgage banks and mortgage brokers. Reads borrower data inside the institution's M365 boundary, governed by Microsoft Entra ID Conditional Access and Microsoft Purview policies. No data leaves the tenant.

Ready to put MortgageExchange, Calyx PointCentral, and Microsoft 365 Copilot to work on pre-qualification?

ABT helps independent mortgage banks, mortgage brokers, and hybrid LO shops on the MortgageWorkSpace footprint pull pre-qualification from weeks to minutes by pairing modern POS interfaces with the MortgageExchange spine, ABT-hosted Calyx PointCentral as the LOS, and Microsoft 365 Copilot Business inside the company's own tenant. Borrower communication automation, audit evidence, and AI governance come standard.

Frequently Asked Questions

Modern POS platforms automate the manual steps that cause the longest delays at intake. They pull credit reports, verify income through services like Plaid, Argyle, and Truv, validate assets in real time, and submit directly to Automated Underwriting Systems. The actual weeks-to-minutes gain, though, depends on what happens after intake. Verified borrower data has to flow from the POS into the LOS and out to the borrower communication channels without anyone re-keying the same field, which is the role ABT MortgageExchange plays inside the mortgage company's integration spine. The POS compresses the borrower experience. The integration spine compresses the rest.

Calyx Path is the desktop product the mortgage company runs locally. Calyx PointCentral is the server edition of Calyx Software's loan origination platform, giving multi-user access across loan officers, processors, and underwriters from a centralized origination environment. ABT hosts Calyx PointCentral on Microsoft Azure for mortgage companies that prefer a Tier-1 Microsoft partner to operate the LOS rather than maintaining it on their own infrastructure. ABT manages the Azure compute and storage, the backup and disaster recovery configuration, and the patching cadence. The mortgage company owns the LOS data and the configuration, and authenticates against the LOS through the same Microsoft Entra ID identity layer that already governs Outlook, Teams, and SharePoint.

Focus on four areas. First, LOS integration depth: does the POS connect through modern APIs with real-time bidirectional sync, and does the mortgage company have a mortgage-aware integration spine like ABT MortgageExchange to carry verified data into the LOS and out to the borrower communication surfaces. Second, actual AI capability: does it reduce loan officer touches in measurable ways, or does it just add a chatbot to the same legacy form. Third, governance posture: does the AI workflow run inside the mortgage company's Microsoft 365 tenant so borrower NPI never leaves the boundary, ideally through Microsoft 365 Copilot Business. Fourth, AUS connectivity: can the POS submit to DU and LPA directly and return findings inside the borrower workflow. Speed without governance is liability with a faster delivery mechanism.

Microsoft 365 Copilot Business runs inside the mortgage company's Microsoft 365 tenant and can read the 1003 application, the income documentation, the asset statements, and the credit report inside that boundary. Copilot produces a structured pre-qualification summary the loan officer reviews and approves, and stages the conditional approval email inside Outlook for the loan officer to edit and send. Copilot is not the underwriter. The pre-qualification decision is still made by a human reviewing the file. The architectural value is that the human is reviewing a structured summary instead of assembling one from five screens, the borrower NPI never leaves the M365 tenant, and the mortgage company can prove with audit evidence what Copilot read, what it summarized, and what the loan officer decided.

Generic middleware platforms route messages between systems, but every mortgage-specific data mapping has to be built and maintained inside the platform by the institution. ABT MortgageExchange ships with pre-built connectors for ICE Encompass, MeridianLink Mortgage, Mortgage Cadence, Dark Matter Empower, and ABT-hosted Calyx PointCentral against Microsoft 365 borrower communication and document surfaces, with the pre-qualification event, the disclosure event, the condition-cleared event, and the closing-package event mapping to mortgage-aware schemas by default. The platform runs on Microsoft Azure, is monitored by ABT, and collects audit evidence on every cross-system handoff. Mortgage companies get the architectural benefit of middleware without the mortgage-specific build burden.

Lenders typically see application-to-pre-qualification time drop from days to minutes for AUS-eligible files, abandonment rates decrease 25-40 percent, and manual touches per loan fall by 60 percent or more. Compliance defect rates drop from 10-15 percent with manual processing to below 3 percent with automation. The durable gain over the first year, though, comes from pull-through rate and the audit posture when Microsoft 365 Copilot Business and Microsoft Purview governance run inside the mortgage company's tenant. Most mortgage companies recover the deployment investment within the first quarter.