In This Article

The average mortgage takes 42 days from application to closing, according to ICE Mortgage Technology's September 2025 data. Meanwhile, the average cost to originate a single loan hit $11,109 in Q3 2025 - 42% above the long-term average - with disconnected workflows driving much of that inflation.

Your Loan Origination System tracks the what. How many loans were processed. Pipeline status. Time to close. But it doesn't tell you why numbers move in the wrong direction. When performance drops, mortgage leaders are left guessing at causes. That guessing costs time, money, and talent.

This article breaks down three specific blind spots that LOS data misses and the real operational damage they cause. If you manage loan processors, underwriters, or loan officers, these gaps are bleeding margin from every file in your pipeline.

This is Part 1 of a two-part series. Part 2: Solving the Blind Spots covers how connected data platforms close these gaps.

What Your LOS Is Not Telling You

Your LOS reports outcomes. Loans closed. Days to close. Pipeline value. These are lagging indicators - they tell you what happened after it already happened.

The leading indicators are invisible. How much time processors spend toggling between systems. Which upstream errors cause underwriting delays. Where loan officers lose hours on tasks that never close deals. A mortgage integration maturity study found that most independent mortgage bankers operate at "Level 1: Fragmented foundations," where systems do not share data and leadership decisions rely on an incomplete picture.

Why Mortgage Leaders Are Flying Blind

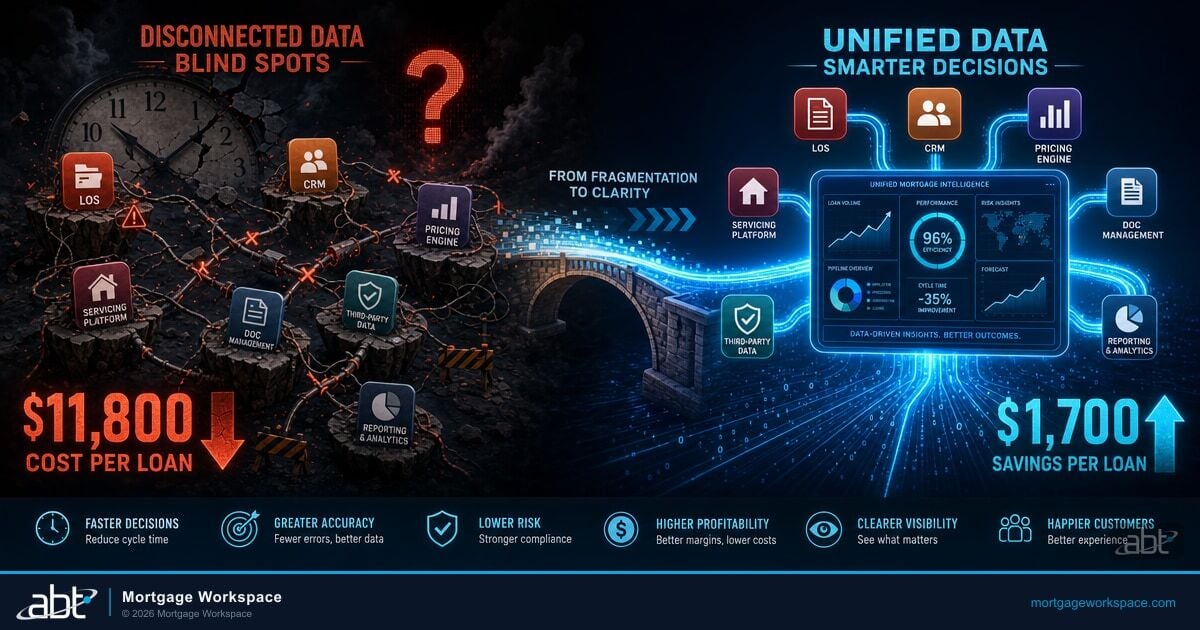

Technology now accounts for 10-18% of operating expenses at large lenders, yet most of that spending goes to individual point solutions - not integration between them. The result: expensive systems that each work well in isolation but collectively leave leadership without the cross-functional visibility needed to diagnose operational problems. You see the symptom but never the cause.

Every mortgage operation runs data in at least four separate places: the LOS, the CRM, employee activity logs, and financial systems. None share data by default. Each gives you a fragment of the picture. Connecting them manually takes hours of pulling reports, aligning formats, and cross-referencing spreadsheets - and that picture is already stale by the time you finish.

Blind Spot 1: The Loan Processor's Hidden Time Drain

Consider a loan processor whose output is falling behind peers. The LOS shows fewer loans processed. It doesn't show why.

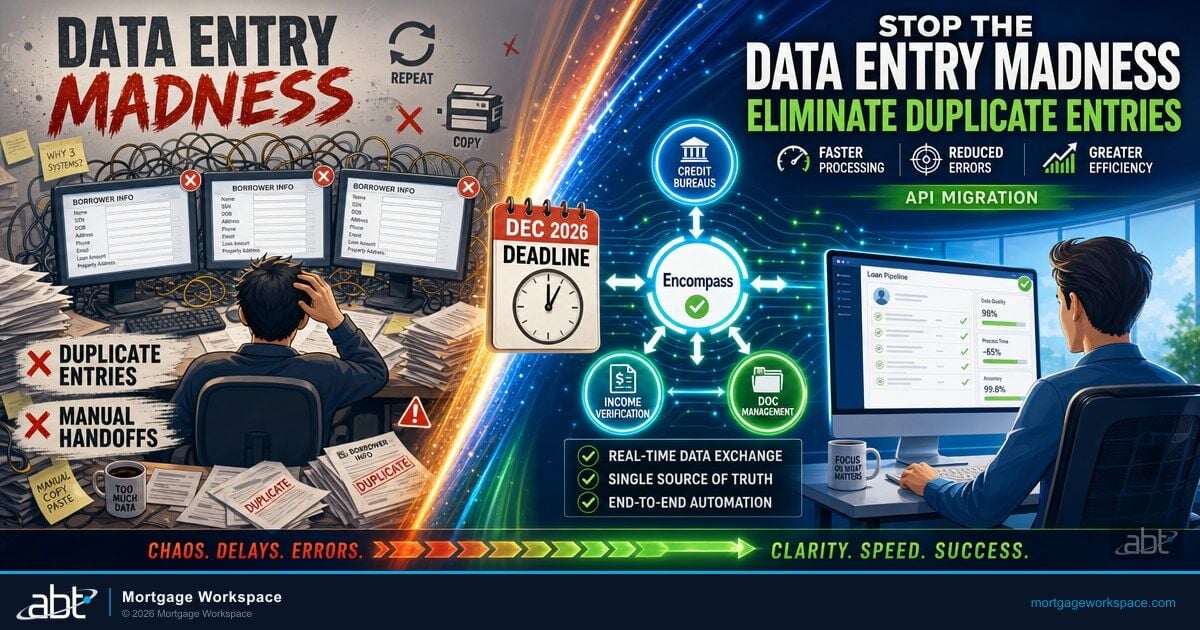

A processor spends 2 to 3 hours per day toggling between Encompass, Outlook, and shared drives - searching for borrower documents in different folders, fixing manual data entry errors that should have been caught earlier, and double-checking compliance requirements across disconnected systems.

Over a month, that adds up to 60 hours of lost productivity - 7.5 full working days spent on tasks that produce zero loan output. Scale that across a team of 10, and you lose 80 hours every week: the equivalent of two full-time employees gone to system friction.

The LOS reports the outcome: fewer loans processed. It never surfaces the root cause - broken workflows between disconnected systems that should be sharing data automatically.

In a market where origination costs already sit 42% above the long-term average, every hour of processor time burned on system friction lands directly on your cost-per-loan. The MBA's Q3 2025 production report shows lenders are actively pursuing technology and process improvements to close this gap - but improvement requires visibility into where the time actually goes.

Blind Spot 2: Why Underwriter Output Drops

A senior underwriter's loan output drops by 50%. Leadership sees the number but not the explanation.

The hidden problem: that underwriter spends her day fixing incomplete loan files. Tracking down missing pay stubs. Correcting inconsistent data across documents. Resolving issues that should have been addressed by processing before the file reached underwriting.

What the LOS Shows

- Underwriter output dropped 50%

- Loan approvals are delayed

- Closing timelines are slipping

- Borrowers are waiting longer

What Connected Data Reveals

- 4 hours/day spent fixing upstream processing errors

- 100 hours/month of lost underwriting capacity per employee

- Incomplete files are the #1 cause, not underwriter performance

- Root cause traces back to disconnected processing workflows

If underwriters spend 4 hours per day fixing upstream errors, that is nearly 100 hours per month of lost underwriting capacity per employee. Multiply across a team, and the reason for slipping timelines becomes obvious - but only if you can see it. Without connected data, leadership is left guessing whether the problem is talent, training, or workload, when the real answer is upstream workflow breakdowns.

Blind Spot 3: The Loan Officer's Stalled Pipeline

A loan officer's conversion rates drop. The LOS shows fewer loans closing. It doesn't explain where the time went.

Here's what the data actually shows: that loan officer spends hours sifting through unqualified leads and handling administrative tasks. Time that should go toward client relationships and closing deals goes to data entry, document chasing, and manual follow-ups that a properly integrated data platform would handle automatically.

Without visibility into how loan officers actually spend their time, leadership invests in more lead generation when the real problem is lead qualification - or blames motivation when the real issue is system friction.

- Fewer deals close because high-value selling time is consumed by low-value administrative tasks

- Pipeline velocity drops as loan officers lose focus on qualified opportunities

- Revenue falls while the root cause stays hidden from leadership and the competitive gap widens

The mortgage tech market is projected to grow at roughly 25% annually through 2032, reaching $35 billion, because lenders are recognizing that these disconnected workflows are unsustainable. The ones who connect their data first will convert more efficiently while competitors continue guessing.

The Real Cost of Siloed Mortgage Data

These four data sources exist in every mortgage operation - and none of them talk to each other:

| Data Source | What It Tracks | What It Misses |

|---|---|---|

| LOS | Loan milestones, pipeline status, closing dates | Why milestones are delayed, where time is spent between events |

| CRM | Borrower relationships, sales pipeline, lead tracking | Whether LOs spend time selling or doing admin work |

| Employee Activity | Time in Encompass, Outlook, and other tools | How that time connects to specific loan outcomes |

| Financial Systems | Revenue per loan, cost per loan, margin analysis | Which operational bottlenecks drive cost-per-loan increases |

Connecting these systems manually means hours of pulling reports, aligning formats, and cross-referencing spreadsheets. By the time you finish, the picture is already stale. Operational losses from this disconnection exceed $1,000 per loan for smaller lenders - a figure that compounds quickly when the MBA projects 5.8 million originations in 2026.

In a market projected to grow only 8% in 2026, margin matters more than volume. The lenders who can identify and fix bottlenecks in real time - through tools like Mortgage BI - will outperform those still assembling manual reports a week after the data expired.

Key Takeaway

Your LOS, CRM, employee activity, and financial systems each hold one piece of the operational picture. Until they connect, you are managing outcomes without understanding causes - and every blind spot costs you money, talent, and competitive ground.

What Comes Next

These blind spots are not permanent. Connected data platforms that unify LOS, CRM, employee activity, and financial data into a single view give mortgage leaders the visibility they need to act on causes, not just symptoms.

Part 2 of this series shows how mortgage companies are connecting their data for faster decisions and measurable results - including how hidden IT complexity costs amplify these data silo problems.

Stop Guessing. Start Seeing the Full Picture.

Mortgage Workspace helps credit unions, banks, and mortgage companies connect their data systems, eliminate manual reporting, and give leadership real-time visibility into operational performance across every role and workflow.

Frequently Asked Questions

Loan Origination Systems track loan-level events: milestones, status changes, and pipeline metrics. They do not track employee activity across other tools like email, document systems, or CRM platforms. When a processor's output drops, the LOS shows the result but not the time spent toggling between systems, chasing missing documents, or fixing upstream data errors that caused the slowdown.

Mortgage companies lose an estimated 8 hours per employee per week to system friction from disconnected tools. For a team of 10 processors, that equals 80 hours per week or the equivalent of two full-time employees worth of lost capacity. Operational losses from data silos exceed $1,000 per loan for smaller lenders with under $100 million in annual volume.

Complete mortgage operational visibility requires connecting four core data sources: the Loan Origination System for pipeline and milestone data, the CRM for borrower relationships and sales activity, employee activity data showing time spent across tools like Encompass and Outlook, and financial systems tracking revenue per loan and operational costs. When these four sources connect, leadership can trace performance issues to their root causes.

Data silos create cascading delays across the loan process. Processors spend hours searching for documents across disconnected systems. Underwriters receive incomplete files and spend time chasing corrections instead of analyzing risk. Loan officers lose selling time to administrative tasks. Each delay compounds through the pipeline, pushing closing timelines beyond the 42-day average and giving competitors with connected systems a speed advantage.